Delayed retirement (5 years and promotion)

Take on a new challenge

If retirement feels like it’s still a few years away yet, and you’re not sure you’ve reached your full potential, maybe a new role with extra responsibility could be a good next step – and a promotion could give your pension a nice little boost too.

To give colleagues an idea of how delaying retirement and taking a promotion could affect pension benefits, we have set out an illustration below which shows how benefits change over time. Details of the contributions that members have to pay to be part of the NHS Pension Scheme are available on the NHS Business Services Authority website.

For our illustration, we’ve used an example of an “officer” member of the NHS Pension Scheme who was age 55 on 1 April 2023 (and so has both 1995 Section and 2015 Scheme benefits). They are currently at band 7 (5+ years’ experience) on the Agenda for Change pay scale and get promoted to band 8a over the coming year

The benefits the member may take at 55 and 60 (accounting for any early payment reductions) are:

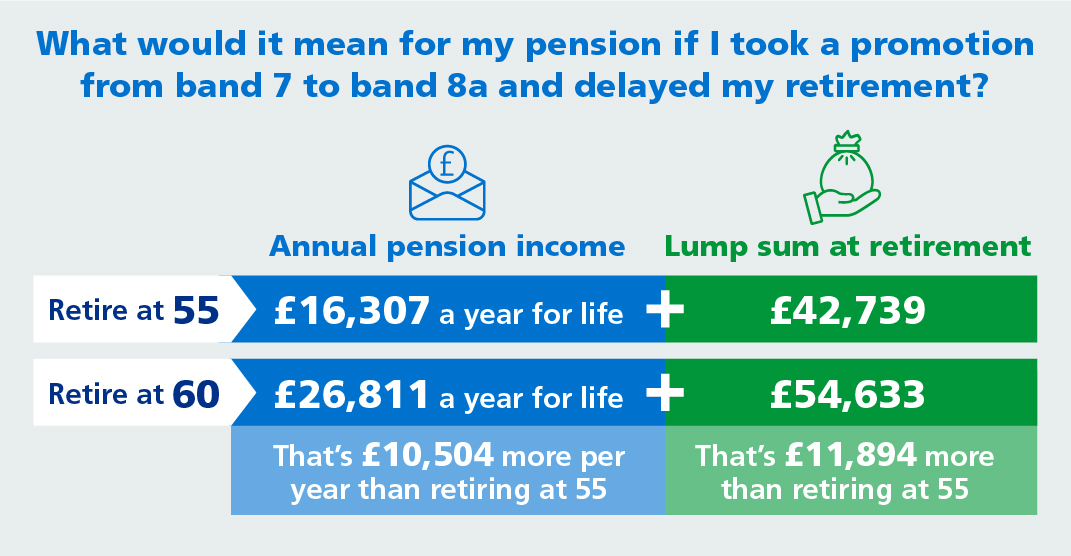

What would it mean if for my pension if I took promotion from a band 7 to a band 8a and delayed my retirement?

| Retire at 55: | £17,720 a year for life | Lump sum of £44,449 |

| Retire at 60: | £29,113 a year for life: That’s £11,393 more per year than retiring at 55 | Lump sum of £57,083: That’s £12,634 more than retiring at 55 |

The member’s benefits have increased because:

- they have built up extra benefits in the 2015 Scheme,

- their past benefits have increased in line with inflation/salary increases (including their promotion), and

- Early retirement reductions are lower for each additional year worked.

An extra note on inflation:

During each year of active service, your 2015 Scheme pension is reviewed to keep in line with the rise in the cost of living. 2015 Scheme pensions are reviewed using the Consumer Price Index (CPI). This measures how costs of a representative basket of goods and services have changed over time. An additional 1.5% is added to this. This makes sure the value of your pension will be above inflation.

Once you start receiving your pension, your benefits will continue to be reviewed each year to keep up with living costs – it’s called the Pensions Increase.

Example assumptions

- The individual is aged 55 as at 1 April 2023.

- The individual was in the 1995 Section of the NHS Pension Scheme until 31 March 2015. They joined the 2015 Scheme from 1 April 2015. The illustrations do not make any allowance for the McCloud judgment, if applicable, for members eventually being given a choice between receiving their legacy (1995 or 2008 Section) and 2015 Scheme benefits in retirement for the period 1 April 2015 to 31 March 2022.

- The individual is an “officer” member. The example does not reflect “practitioner” benefits.

- The individual has a pensionable salary of £47,672 (Band 7) before their promotion. Their salary after promotion is £50,224 (Band 8a). Salary increases for 2023/24 are assumed to be 3.5% and then 2% p.a. thereafter.

- The illustrations are based on the current actuarial factors in force in the Scheme (August 2021) – these are used for calculating any reductions to benefits because benefits are paid prior to Normal Pension Age. In the 1995 Section, benefits paid after Normal Pension Age (60) are not subject to increases for late payment and so individuals staying beyond Normal Pension Age need to consider this when assessing their options.

- The member does not have Special Class status or Mental Health Officer status – therefore, their 1995 Section benefits will be reduced to reflect the fact that they’re being paid before Normal Pension Age prior to age 60. Individuals with Special Class status or Mental Health Officer status may be able to draw their benefits earlier without these reductions applying. See the NHS Business Services Authority website for more information about Sspcal Cclas status and Mental Health Officer status. Specifically, it is important to consider whether changes in roles will have an impact on Mental Health Officer or Special Class status.

- The illustrations do not allow for the uptake of certain options that members may be able to exercise, for example, they do not allow for the exchange of pension for additional cash.

- The figures quoted may incorporate a small degree of rounding.

- All of the examples are illustrative only and are not designed to represent the particular circumstances of any one individual. Find out which pension scheme you are a member of on the NHS Business Services Authority website.

See below for more detail:

The benefits the member may take at 55 (accounting for any early payment reductions) are:

| Retire at 55 | 1995 Section | 2015 Scheme | Total |

| Service | 28 | 7 | 35 |

| Pension | £13,348p.a.* | £4,372 p.a.** | £17,720 p.a. |

| Lump sum | £44,449*** | – | £44,449*** |

The benefits the member may take at 60 (accounting for any early payment reductions) are:

| Retire at 60 | 1995 Section | 2015 Scheme | Total |

| Service | 28 | 12 | 40 |

| Pension | £19,028p.a. | £10,085 p.a.** | £29,113 p.a. |

| Lump sum | £57,083 | – | £57,083 |

* includes early retirement adjustment of 20% at 55.

** includes early retirement adjustment of 43.7% at 55 and 30% at 60.

*** includes early retirement adjustment of 11.2% at 55.

Talk to your manager to find out more about your flexible working options.

See your personal pension details on your Total Reward Statement

Looking for more flexible working options?

- Change your hours or use your skills differently for a better work/life balance

- See if retiring and coming back in a different role could work for you

- Stay with the NHS for a little longer and see if you could get more from your pension

- See our frequently asked questions and helpful links to find out more