We've put some small files called cookies on your device to make our site work.

We'd also like to use analytics cookies. These send information about how our site is used to a service called Google Analytics. We use this information to improve our site.

Let us know if this is OK. We'll use a cookie to save your choice. You can read more about our cookies before you choose.

Financial accounting updates — International Financial Reporting Standard 16 Leases implementation

Application of IFRS 16 to the measurement of PFI liabilities

Application of IFRS 16 measurement principles to PFI liabilities is effective from 1 April 2023.

DHSC PFI accounting model – updated for IFRS 16 (updated 15 December 2023)

In 2009 DHSC procured a national PFI model to support the transition to IFRS in the NHS. DHSC has updated this model to incorporate remeasurement of PFI liabilities under IFRS 16 from 1 April 2023.

Guidance on International Financial Reporting Standard (IFRS) 16 on Leases for NHS providers and commissioners. IFRS 16 was implemented in the NHS from 1 April 2022.

DHSC Group Accounting Manual (GAM) 2022/23

The DHSC GAM for 2022/23 contains guidance on the application of the standard for the NHS.

Our updated IFRS 16 implementation guide pulls together various sources of guidance and includes a timetable with milestones for IFRS 16 implementation. It also provides further details of individual tasks and national exercises that will support implementation of the Standard.

This Powerpoint IFRS 16 Implementation Slide Deck from DHSC is a training slide deck that explains principles of the IFRS 16 and how accounting for leases changes under the new standard. It has been developed with finance and operational/commercial users in mind, to help colleagues assess the impact of IFRS 16 on accounting, budgeting and operations.

DHSC example lease register

This example lease register from DHSC is for recording of leases from the perspective of a lessee. This example register may be useful to entities that are considering what level of data is required to be collected to inform the accounting and budgeting entries for each lease, or have not yet developed a lease register or finalised a systems approach. It is shared for information purposes and does not form part of a mandatory data collection requirement.

DHSC lease accounting tool – updated 9 December 2022

This DHSC lease accounting tool is a spreadsheet tool developed by DHSC which helps to calculate and summarise liability and asset values under IFRS 16 for each lease entered in the tool. It is optional for use.

Please read the guidance in the workbook – some limitations of the tool are explained as tips with yellow stars.

Users may wish to avoid re-using the lease numbers that now contain worked examples as some of the formulas on the detail calculation sheets have been overwritten to reflect subsequent remeasurements in those examples.

If the tool is used for existing operating leases transitioning on 1 April 2022, please enter the start date for the lease term as 1 April 2022 and do not enter a rate implicit in the lease as the the HM Treasury incremental borrowing rate should be used for all previous operating leases on transition.

Further update 16 December 2021: The HM Treasury incremental borrowing rate has been updated to 0.95%, as confirmed by HMT in December 2021.

Update 9 December 2022: Error in the allocation of future lease payments to maturity bands corrected

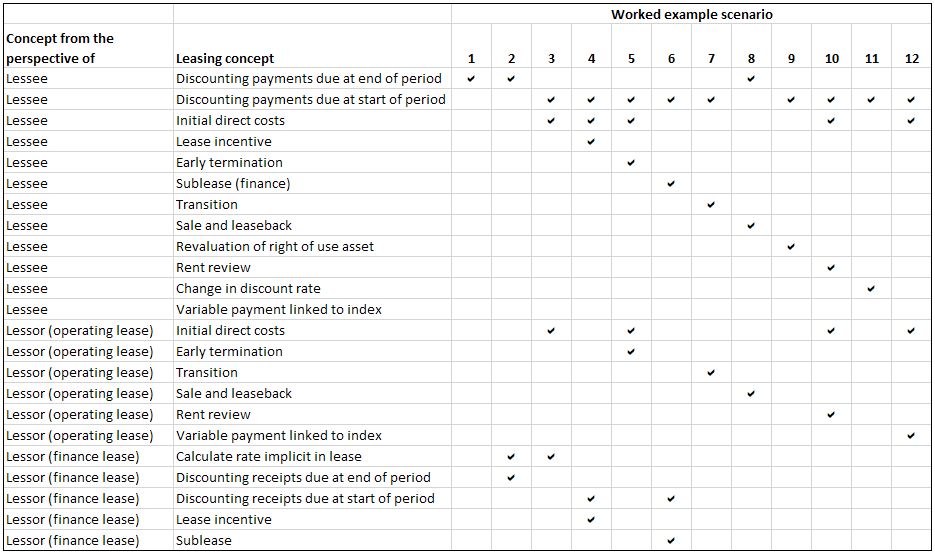

DHSC worked example spreadsheets

DHSC has developed a series of worked examples that illustrate the calculation of lease accounting entries and the impact on accounts in each scenario.